{kind=link}

- FOMC minutes likely to be seen as out-of-date following recent soft data

- But hawkish surprise can still jolt markets as Fed rate cut bets seem overdone

- Can the minutes due Tuesday (19:00 GMT) offer the bruised dollar some support?

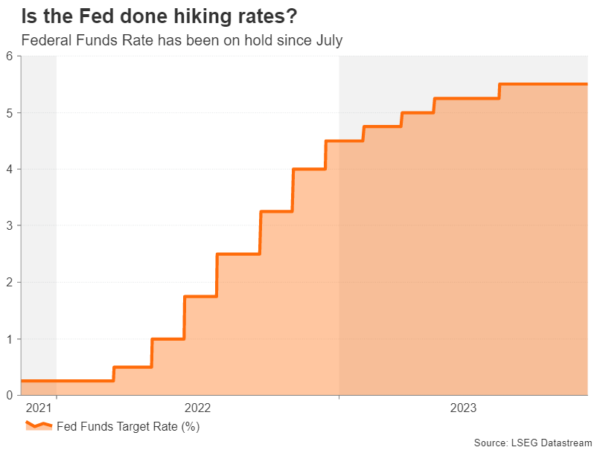

Fed on pause

When the Fed decided to keep interest rates unchanged at its October 31-November 1 meeting, it came closer than it has done during this tightening cycle to signalling that it is done hiking. Although the decision came hot on the heels of the Q3 GDP report that showed the US economy grew by a staggering 4.9% annualized pace, Chair Jerome Powell pointed to the recent tightening of financial conditions as cause for caution.

The data since that meeting has gone somewhat south, including inflation, further corroborating the view that no more tightening is needed. So, is there any reason to believe that the minutes will dash hopes of a Fed pivot? The answer is, probably not. But the minutes may nevertheless rein in expectations of how soon or how aggressively the Fed will slash rates in 2024.

The elusive pivot

The problem for the markets is that they’ve been wrongly pricing in a dovish pivot over the past year and each time the Fed has had to double down on its higher for longer stance, triggering a massive rebound in the US dollar and panic selling on Wall Street. This time, the markets may be right, as even the most hawkish FOMC members are questioning whether additional tightening will be required.

The danger is that investors are interpreting the message of peak rates not simply as the end of rate hikes but also the start of a rate cutting cycle. It can be argued that markets are somewhat less optimistic about the growth outlook than the Fed is. Although the strong gains in the stock market this year and particularly since the November meeting would suggest otherwise, it’s worth noting here that when excluding the Magnificent 7 from the equation, Wall Street’s performance hasn’t been that impressive.

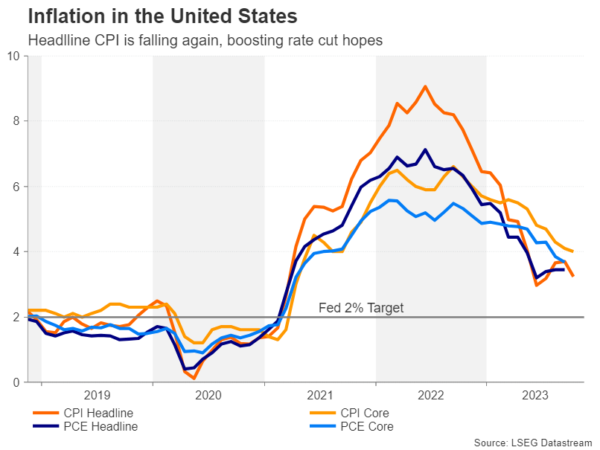

Inflation is falling, but for how long?

But what about the data? The latest inflation figures have been encouraging. Headline CPI fell for the first time in four months in October, hitting 3.2%, and core CPI eased too. The Fed’s preferred core PCE measure has also continued to come down. With oil prices taking a tumble lately, there’s not a significant risk of energy costs driving up inflation again over the coming months. But the progress in bringing down inflation is slowing and may even stall before the 2% target is met. One worry is that services inflation may become sticky.

Looking at other indicators such as the weakness in global manufacturing and growing evidence that the US labour market is finally cooling, the risks to inflation seem tilted to the downside. Jobless claims have been steadily rising over the last few weeks and wage pressures are moderating too.

Markets think the Fed will cut rates by 100bps in 2024

All this has prompted investors to price in almost one full percentage point of rate cuts next year, sending Treasury yields sharply lower. The 10-year yield has plummeted from a high of 5.02% in October to around 4.45% currently. The more than 50-basis-points drop in a single month weakens the argument that tighter financial conditions are doing the job of additional rate hikes by the Fed and the minutes may well stress that point.

If policymakers talk up the economy in the minutes and remain unconvinced about inflation returning to the 2% target within a reasonable timeframe, investors may pare back some of their rate cut bets, especially in the absence of any top tier data during what is expected to be a quieter trading period due to the Thanksgiving break on Thursday.

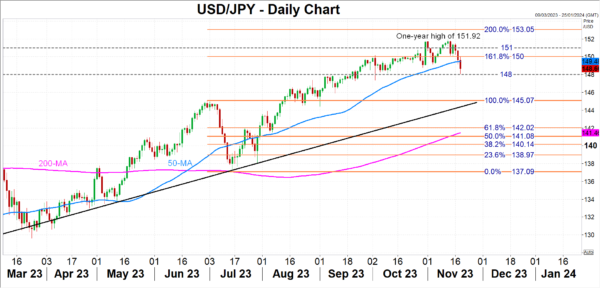

Dollar could get volatile during holiday week

In such a scenario, the dollar may reverse higher, reclaiming its 50-day moving average against the yen in the 149.50 region and attempt to surpass November’s one-year peak of 151.92.

However, if the minutes strike a neutral tone, this would be seen as endorsing the market pricing for rate cuts, potentially pulling the dollar below the 148.00 yen level and towards the June top near 145.00.

On the data front, traders will be keeping an eye on October durable goods orders as well as the latest weekly jobless claims on Wednesday, while on Friday, attention will turn to S&P Global’s flash PMI estimates for November.