{kind=link}

- The Fed maintained monetary policy unchanged in the November meeting as widely anticipated. We still think the Fed’s rate hikes are already over.

- Powell underscored, that the tightening in financial conditions needs to be persistent to influence monetary policy, but also that policy is already restrictive.

- EUR/USD rose around 50 pips, while 10y US Treasuries extended their rally with yields declining by 17bp throughout the session.

Powell delivered a balanced message with dovish undertones, as even the statement made it clear that the Fed is now closely following changes in financial conditions. Powell emphasized, that the rise in long-end yields needs to be both persistent and driven by higher term premium to influence monetary policy, but also that policy is already restrictive today.

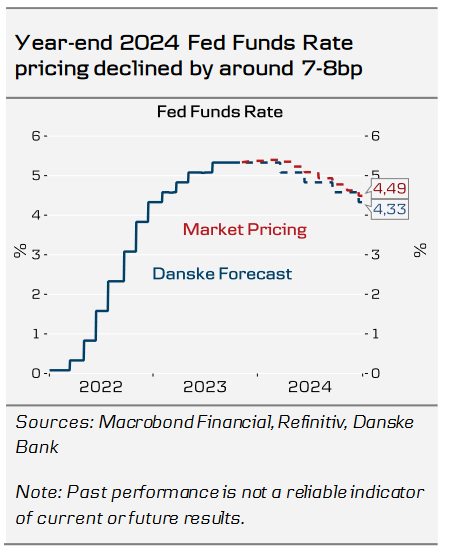

The Fed is not considering any changes to QT due to higher bond yields, as ‘reserves are not even close to scarce at this point’, which is in line with our thinking as well. We expect the Fed to continue QT at least into late 2024, and in any case well past the first rate cut, which we continue to pencil in for next March.

On the macro front, Powell chose to emphasize more balanced labour markets and cooling wage growth. Despite the recent upticks in both consumer survey and market-based inflation expectations measures, Powell was optimistic that inflation expectations remain ‘in a good place‘. In other words, while the recent upside data surprises provided Powell an option to deliver a more hawkish message, he did not consider it necessary.

As we also discussed in our Fed preview, 25 October, Powell noted that the lags of monetary policy transmission could be longer than before, as refinancing at higher rates will push companies’ net interest costs higher gradually over the coming years. Following the weaker ISM Manufacturing survey for October, Atlanta Fed’s GDP nowcast declined to 1.2%, down from the previous estimate of 2.3% and 4.9% growth in Q3. While we generally avoid putting too much emphasis on a single nowcast model, Atlanta Fed’s estimate foresaw the acceleration in Q3 GDP clearly before analyst consensus. Housing and business investments are already responding to higher interest rates, and we still expect private consumption to follow suit towards the winter. As we see growth risks tilted to the downside, we stick to our call that the Fed is already done with rate hikes for now.

Markets: Persistence is the key

The cautious signals from Powell accelerated the decline in long US yields, which started earlier today following the release of the less dire than expected quarterly refunding statement and disappointing ISM Manufacturing. 10Y UST yields are down 17bp for the session, while the short end of the curve is less changed. Today’s massive bond market rally underlines, why Powell mentioned the persistence of the move up in long yields as a key factor in terms of evaluating the economic impact. EUR/USD edged up by approximately 50 pips and we maintain our near-term bias for higher EUR/USD on the back of a turnaround in the exceptional run of positive US economic data surprises. On the longer horizon, we forecast EUR/USD at 1.06/1.03 in 6/12M.